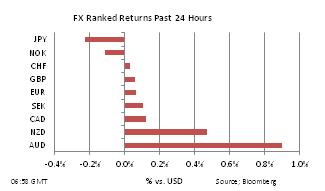

The big question this morning for markets is whether to meet the latest Chinese GDP data with concern that it was lower than expected, or relief that the economy is slowing in an orderly fashion and will be supported by the largest increase in yuan-lending for a year. The initial reaction, as suggested by the Aussie's movement, is that concerns are more about the slower than expected pace of growth, AUD down around 0.5% in the wake of the release. The yen is also the only leader vs. the dollar after the numbers. Also seen were modestly firmer industrial production numbers for March (11.9% YoY) and retail sales figures, which were in line with expectations at 14.8%. China is juggling a lot of balls right now, trying to slow the economy a little, rebalance it towards consumption, ensure that property prices soften rather than crash and control lending so it does not fuel potential new bubbles. For now, it looks like policy-makers are achieving their goals but it's a precarious balance.

Also in today's Daily Forex Brief:

- Monti's continuing battle

- Housing still a big US headwind

- The impending franc attack