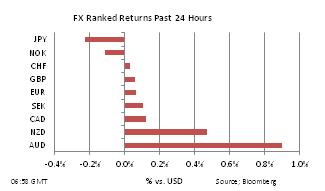

It has been exceedingly gradual, but the dollar has been drifting downwards over the past two weeks. Not that we are talking about a big move mind you – the dollar index is down by roughly 1.5% over that time. That said, some of the major dollar crosses are at levels not witnessed for some time – cable for instance reached a 7mth high at just under 1.63 overnight. Indeed, the pound has been something of a revelation so far this year, despite the fact that the economy is apparently back in recession. Clearly sterling is attracting flows from a number of different sources. Just imagine how well the currency might be doing if the economy was actually registering the kind of growth that America is experiencing. The Japanese yen is also faring quite well, after a torrid period in February and the first half of March. Even the beleaguered Aussie has perked up, despite mounting speculation that the RBA will cut rates by 50bp by mid-year. All things considered, it has been an indifferent first four months of the year for the dollar, which is slightly surprising as the economy looks better than most, corporate earnings are healthy and the Fed has backed away from implementing further QE after Operation Twist finishes next month. Part of the explanation is that there has been a slight improvement in risk appetite recently. For now, some of the high-beta currencies such as the Kiwi and the ZAR are attracting interest, while sterling retains a very healthy bid.